Beijing’s Currency Wishlist

The Financial Times reporting on a recent essay in the CCP’s leading ideological journal Qiushi that Xi Jinping had called for China’s currency, the renminbi, to be a “powerful currency” and one which could be “widely used in international trade, investment and foreign exchange markets, and attain reserve currency status”. And why should he not? China is a trading powerhouse with the world’s second largest economy, and factory to the world for an increasing number of low-tech and hi-tech goods. And it’s not as if this call for a bigger role for the renminbi in global financial markets is new. Even Xi’s remarks date back to 2024 but calls for a prominent role for the currency have been made for decades but still the renminbi has failed to reflect the vast changes and status of the Chinese economy over that time. And neither are Xi’s comments in isolation, a number of other domestic economists have made similar calls to broaden the appeal and use of the renminbi but speeches can do little to tackle the very real problems which have held back renminbi usage.

Although there have been calls for the renminbi to be used broadly Chinese officials often played down the role of the renminbi and instead talked about the dangers of being too dependent on the dollar. They didn’t want to be too forceful in promoting their own currency knowing that they simply were not in a position to assume the dollar’s global role. But now Xi is indicating that he is more confident to promote this currency especially as he sees Trump effectively trashing his own currency and making the US a less safe business and investment environment. It is important to remember as well that the discussion isn’t just about what the actual renminbi to dollar exchange rate is, that will fluctuate for a slew of reasons. The goal for the Chinese is to have their currency assume a significant role across both denominating and settling both trade flows and financial flows.

The Long Torturous Path of Limited Reforms

During the 90s and following China’s ascension to the WTO the primary concern around China’s currency was whether it was undervalued or not. Many countries in Asia had restricted capital controls and their currencies were pegged to the dollar. The certainly of such pegs resulted in excessive dollar borrowings which became unstuck with the Asia Financial Crisis of 1997. Beijing saw the economic chaos which the AFC wreaked across Asia and was determined that they could not let themselves become subject to such violent cross border flows. That mindset still broadly remains.

Following WTO entry the discussion was whether Beijing was unfairly manipulating its currency, i.e. keeping it too weak to support their export markets. Indeed, how could post-WTO China be selling so much and attracting so much money, yet the currency fails to move? Only in 2005 did Beijing move away from the fixed 8.3 renminbi to the dollar and slowly let the currency appreciate to an eventual high of 6.1 about a decade later.

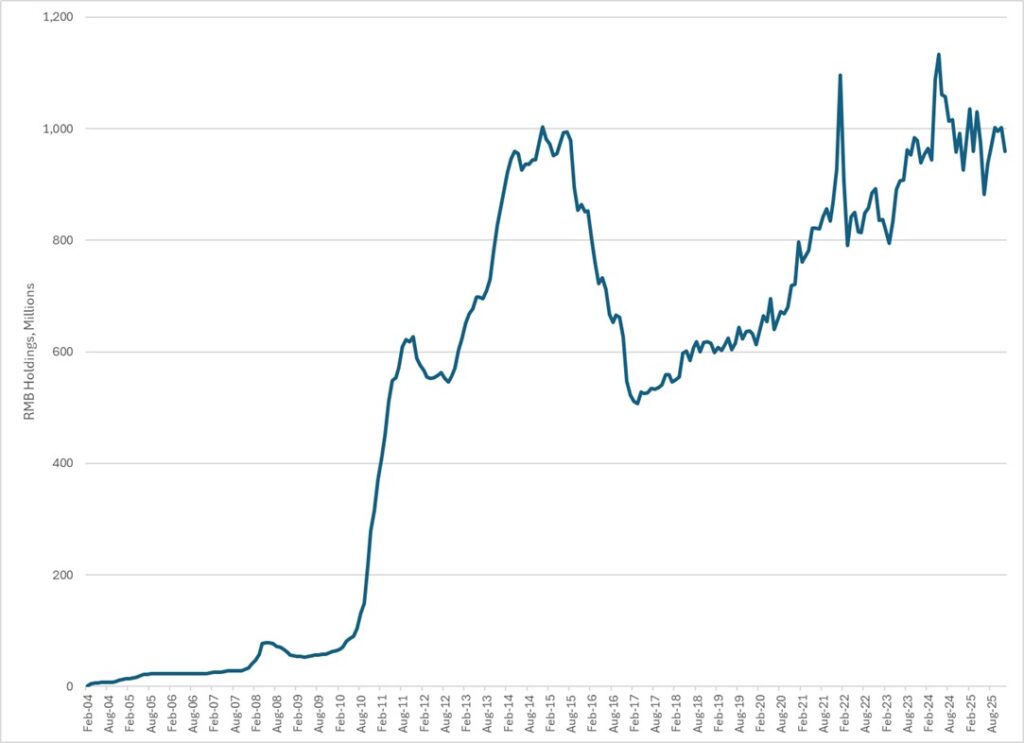

The first real move to open up capital account flows (the current account had been convertible since the mid-90s) only happened in 2010 with the PRC authorities allowed HK corporates to open RMB accounts in the territory and remove restrictions related to transfers between accounts. As the chart below shows this led to massive growth in the pool of renminbi funds which totaled a trillion renminbi in late 2014 but largely failed to grow beyond that level even a decade earlier. As of the most recently HKMA figures HK dollar and US dollar deposits in Hong Kong still account for 88% of all deposits.

A decade ago also saw the IMF accept the RMB into their SDR, Special Drawing Reserve basket after heavy Chinese lobbying. This is not a currency but an IMF defined and maintained international reserve asset which countries can use to supplement their reserves. The inclusion raised eyebrows at the time as the renminbi usage and openness in real financial markets remained extremely limited.

Total Renminbi Deposits in Hong Kong

Source: HKMA

Running parallel to the currency rate and HK account moves Chinese domestic capital markets in both stocks and bonds boomed. Equity issuance grew dramatically especially across non-state sector companies and bond issuance exploded as local governments scrambled to fund the vast stimulus which was unleased post the global financial crisis. In part to fund that growth, and to try and better price the associated risk the Chinese regulatory authorities expanded a range of specific programs to allow direct investment in domestic listed stocks and bonds. So, while there was certainly movement in opening the capital account the measures were generally limited in scale and scope. Approvals for the type of investor, the type of security and the amount invested were common. The currency great wall even when missing a few bricks, or with a small window or door still remains a great wall.

One area where China has had some success in developing the renminbi as a default currency is in trade into Hong Kong between Chinese companies and also with the economic lifeline it provides to Russia. In both cases Beijing has been able to dictate that trade be denominated and settled in RMB although they have had failed to replicate that with other countries. Even globalization with Chinese characteristics, i.e the Belt and Road Initiative has had limited success is using renminbi as the default currency.

This then is the current patchwork of renminbi usage and acceptance. What does Xi need to do to achieve his renminbi goals?

Politics and Economics in Conflict

It is not surprising that Xi Jinping is promoting the renminbi and dangling yet again the carrot of reform to try and encourage foreign capital to invest again into China. Trump’s ever more erratic behaviour towards US allies and the Supreme Court’s ruling on the illegality of his “Liberation Day” tariffs reinforce how uncertain a market the US has become. Xi has tried to exploit this by welcoming many foreign leaders to Beijing and promoting China and Chinese trade as a place of stability.

Some commentators further suggest that China has already started to pivot away from the dollar and it is only a matter of time before the renminbi dethrones the greenback. The evidence for this is that even with a trillion-dollar trade surplus China’s official foreign exchange reserves have not moved to reflect these trade flows. The explanation of his mismatch strikes at the heart of the Chinese financial system weaknesses. Brad Setser, a former US treasury official and long-time follower of China’s financial flows shows these flows are no longer flowing through the central state entities like the foreign exchange administrator but instead being reflected in the balance sheets of the state-owned banks. For decades the Chinese authorities have been adept at hiding or disguising financial flows by employing a cast of central authority or state-owned entities. While the big state banks are listed and need to disclose balance sheets many others entities are either entirely unknown or their balance sheets are opaque, even assuming that such reporting is honest.

Here then is one of the key reasons China has had such problems in developing the renminbi as a global currency. If a country or company ends up owning balances in renminbi it needs a place to invest them and the Chinese financial markets remain opaque. The scale of the domestic markets is huge if one were just to look at issuance figures in terms of issuing entities or value issued but many of the issuers are largely unknown with little disclosure and very little chance of finding things out. Under the Chinese system, finance, like everything else is subordinate to politics. Central government dictates that there is a stimulus which the local governments need to pay for and bankers and financiers go into overdrive to create innovative ways to raise funds and move the proceeds around. Paying back those funds is a problem for later.

Economic commentators may lament and warn against Trump’s attacks on the Federal Reserve and its independence but surely on one can think that the Peoples Bank of China is free of political interference? China financial system it intimately interlinked with politics, it can be no other way. Unravelling, if that is even the correct word, the links and network of political, financial, central government and local governments ties throughout the domestic economy it’s just “reform and opening”, it is a complete rejection of the current system.

The other key weakness of the renminbi is that it remains controlled. It remains controlled at a daily market movement level where the PBOC set a daily fixing level around which the currency can trade, and then the blunter weapon of the currency great wall which remains firmly in place. The lesson taken from the Asian Financial Crisis is as relevant now as it was then. China saw how foreign capital flows could destabilize domestic markets and then economies, the idea that “a fund manager presses a button in New York and a billion dollars leaves Thailand” had devastating consequences for Thailand in the late 90s and Beijing doesn’t want to expose itself to such violent shocks. In China’s case though the concern is more than middle class and wealthy Chinese will move much of their savings out of the country to better returns and better legal protections outside of China. Either way, the one-party state cannot continue without the protection which a close capital account brings.

The opacity and financial legerdemain which has resulted in the world’s largest banking system is simply not fit for purpose to handle the flows which would come with the renminbi displacing the dollar. Under the present conditions the system can function and provide a return on renminbi assets but the ability to open up the system and compete with the dollar, or the euro, on a like for like basis is just unworkable.

If the weaknesses of the financial system are not enough to limit the renminbi’s rise, then the trillion dollar plus trade surplus doesn’t help. While it is not impossible for reserves to be built up in a surplus currency it certainly makes it much harder especially as Chinese purchases of real assets are treated with suspicion by many developed countries.

Xi Jinping is confronted by what really is an insoluble problem. He sees the opportunity which a reckless and chaotic US brings yet he ultimately doesn’t have the capacity to step into the gap. He can certainly try and squeeze out better trade terms with some countries, and he has already used his leverage in the rare earth elements area, but his economy and financial system just cannot replace the US and the dollar. His financial markets are opaque, littered with worthless issuance, and certainly not deep enough and liquid enough to handle true reserve status. His economic policy of self-sufficiency and export driven growth has resulted in frighteningly large surpluses which both developed and global south countries are desperate to protect themselves from. Even areas of success such as EVs are islands of excellence in a sea of waste funded by the very issuance which is now worthless.

Xi has dreamed big for China, but the economic reality is much bleaker. This doesn’t mean collapse is around the corner, but neither is replacing the dollar or the US. Muddling through behind the safety of capital controls and creative accounting is the best Xi can achieve. It’s not his China Dream but it isn’t a nightmare either.

Privatizing China: Inside China's Stock Markets

by Fraser J. T. Howie (Author), Carl E. Walter (Contributor)

Red Capitalism: The Fragile Financial Foundation of China's Extraordinary Rise

by Carl Walter (Author), Fraser Howie (Author)

カテゴリー

最近の投稿

- The New Oil Power

- From Black Ships to White Hulls: Taiwan–US Coast Guard Imagery and the Transformation of Indo-Pacific Maritime Order

- 中国では「碰瓷(当たり屋)」と嘲笑 日本が「対話があった」かのように報道する日中外相の通りすがり接触

- Mechanisms Advance, Strategy Stays Restrained: ASEAN’s Manila Meeting and the Institutionalisation of South China Sea Competition

- 習近平はどう出るのか? イラン再攻撃をするトランプの背後でうごめいていた米軍の秘密戦略

- 中国のネットで沸く高市X投稿「風呂掃除、洗濯、裁縫、アイロンかけ…」

- トランプ大統領令「国防企業への中国の影響力排除」はG2構想を崩すか?

- 高市内閣支持率41% 中国は支持率下落をどう見ているか?

- トランプ演説の「中国の2020米大統領選介入」対中批判はG2構想を崩壊させるのか?

- GDPでは測れない中国の新産業(ハイテク製造業)生産力